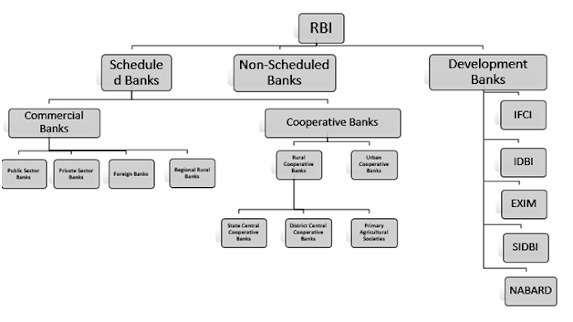

#Reserve Bank of India is the central bank of the country and regulates the banking system of India. The structure of the banking system of India can be broadly divided into scheduled banks, non-scheduled banks and development banks.

Banks that are included in the second schedule of the Reserve Bank of India Act, 1934 are considered to be Scheduled banks.

All scheduled banks enjoy the following facilities:

- Such a bank becomes eligible for debts/loans on bank rate from the RBI

- Such a bank automatically acquires the membership of a clearing house.

All banks which are not included in the second section of the Reserve Bank of India Act, 1934 are Non-scheduled Banks. They are not eligible to borrow from the RBI for normal banking purposes except for emergencies.

Scheduled banks are further divided into commercial and cooperative banks.

1.Commercial Banks

The institutions that accept deposits from the general public and advance loans with the purpose of earning profits are known as Commercial Banks.

Commercial banks can be broadly divided into public sector, private sector, foreign banks and RRBs.

i. Public Sector Banks-

the majority stake is held by the government. After the recent amalgamation of smaller banks with larger banks, there are 12 public sector banks in India as of now. An example of Public Sector Bank is State Bank of India.

ii. Private Sector Banks -

are banks where the major stakes in the equity are owned by private stakeholders or business houses. A few major private sector banks in India are HDFC Bank, Kotak Mahindra Bank, ICICI Bank etc.

iii. A Foreign Bank -

is a bank that has its headquarters outside the country but runs its offices as a private entity at any other location outside the country. Such banks are under an obligation to operate under the regulations provided by the central bank of the country as well as the rule prescribed by the parent organization located outside India. An example of Foreign Bank in India is Citi Bank.

iv. Regional Rural Banks-

were established under the Regional Rural Banks Ordinance, 1975 with the aim of ensuring sufficient institutional credit for agriculture and other rural sectors. The area of operation of RRBs is limited to the area notified by the Government. RRBs are owned jointly by the Government of India, the State Government and Sponsor Banks. An example of RRB in India is Arunachal Pradesh Rural Bank.

2.Cooperative Banks

A Cooperative Bank is a financial entity that belongs to its members, who are also the owners as well as the customers of their bank. They provide their members with numerous banking and financial services. Cooperative banks are the primary supporters of agricultural activities, some small-scale industries and self-employed workers. An example of a Cooperative Bank in India is Mehsana Urban Co-operative Bank.

At the ground level, individuals come together to form a Credit Co-operative Society. The individuals in the society include an association of borrowers and non-borrowers residing in a particular locality and taking interest in the business affairs of one another. As membership is practically open to all inhabitants of a locality, people of different status are brought together into the common organization. All the societies in an area come together to form a Central Co-operative Banks.

Cooperative banks are further divided into two categories - urban and rural.

i. Rural cooperative Banks are either short-term or long-term.

Short-term cooperative banks can be subdivided into State Co-operative Banks, District Central Co-operative Banks, Primary Agricultural Credit Societies.

Long-term banks are either State Cooperative Agriculture and Rural Development Banks (SCARDBs) or Primary Cooperative Agriculture and Rural Development Banks (PCARDBs).

ii. Urban Co-operative Banks (UCBs) refer to primary cooperative banks located in urban and semi-urban areas.

3.Development Banks

Financial institutions that provide long-term credit in order to support capital-intensive investments spread over a long period and yielding low rates of return with considerable social benefits are known as Development Banks. The major development banks in India are; Industrial Finance Corporation of India (IFCI Ltd), 1948, Industrial Development Bank of India' (IDBI) 1964, Export-Import Banks of India (EXIM) 1982, Small Industries Development Bank Of India (SIDBI) 1989, National Bank for Agriculture and Rural Development (NABARD) 1982.

Conclusion :

The banking system of a country has the capability to heavily influence the development of a country’s economy. It is also instrumental in the development of rural and suburban regions of a country as it provides capital for small businesses and helps them to grow their business. The organized financial system comprises Commercial Banks, Regional Rural Banks (RRBs), Urban Co-operative Banks (UCBs), Primary Agricultural Credit Societies (PACS) etc. caters to the financial service requirement of the people. The initiatives taken by the Reserve Bank and the Government of India in order to promote financial inclusion have considerably improved the access to the formal financial institutions. Thus, the banking system of a country is very significant not only for economic growth but also for promoting economic equality.g

Comments

Post a Comment